If you have any questions or would like to get in touch, submit a call back request and our team will contact you as soon as possible or call us on 020 7499 6424 or email us at [email protected]

07 December 2023 -

Investing

Glass half empty or full?

Outlook 2024

In summary

As we near the end of 2023, we are at a crossroads for both economies and investments. During 2023 sentiment has oscillated between two different investment scenarios, the glass-half-full camp, and the glass-half-empty camp. The challenge is to construct portfolios while recognising that either scenario could occur. Given the uncertainty which prevails, we believe that maintaining a balance is key.

2023 has been a year in which investment markets have encountered cross winds. On the positive side, equity markets have benefited from a new age in technology, driven by generative artificial intelligence (AI). At the same time, geopolitical risks have heightened with Russia’s ongoing invasion of Ukraine alongside the conflict in the Middle East between Israel and Hamas. Furthermore, China-US relations remain fraught, despite recent efforts to improve them.

Inflation is the key focus for policy makers and with interest rates clearly in restrictive territory, the glass-half-empty camp is waiting for the full impact of higher interest rates on consumers and companies. At the same time, any worsening of the situation in the Middle East or tightening of supply by the OPEC+ members would lead to a rise in the oil price, causing further upward pressure on inflation.

The glass-half-full camp believe that given labour markets remain tight, wage growth will be robust. In the US, many consumers still have post-pandemic savings to spend and unlike in the UK, for example, have 30-year fixed rate mortgages meaning they are insulated from the recent rate rises.

The key question for both camps is whether consumers and companies will remain solvent while policy makers wait for inflation to fall back to the Central Banks’ targets.

How did we get here?

After a tough 2022 when both equities and bonds posted negative returns, 2023 has seen a recovery, at least in equity markets. At the time of writing, government bonds are still in negative territory, despite the fall in yields (and corresponding rise in prices) seen since the peak of mid-October. The MSCI All Country World Index is up 10.4% in total return, sterling terms. However, the same index adjusted on an equal-weight basis (where each stock has an equivalent weight in the index, removing the dominance of so-called ‘mega-cap’ stocks), is down -1.4%. This difference highlights the impressive performance of a small number of technology-related names which are perceived to be beneficiaries of AI.

The age of Generative AI

The new age of AI started with the launch of Chat GPT in November 2022. Chat GPT is what is known as a large language model-based chatbot developed by Open AI, enabling users to generate media (be it text, code, pictures and more). By January 2023 it had over 100 million users per month and was the fastest growing consumer software application in history. Investor attention turned to companies believed to be the enablers of AI, particularly those focused on designing the necessary semiconductors: Nvidia, the US chip designer, has risen by comfortably more than 200% year to date. The key question is the size of the productivity gains across the broader economy. The US National Bureau of Economic Research looked at a staggered introduction of a generative AI-based conversational assistant using data from over five thousand customer support agents and found that access to the tool increased productivity, as measured by issues resolved per hour, by 14% on average. Clearly gains of this magnitude will help mitigate the effects of higher interest rates and wage costs.

Corporate earnings growth remains robust

After the boost from the post pandemic recovery, corporate earnings growth expectations are lower but still in positive territory. Data from Factset indicates that companies are delivering better than expected earnings-per-share numbers at an historically high rate. Looking ahead to 2024, current consensus estimates point to an expected annual US company earnings growth rate of over 11%. The operating environment is also becoming more favourable: post pandemic supply chain disruptions have ceased and trade volume growth of 3.3% in 2024 is expected, compared to 0.8% in 2023*.

Economic growth picture still mixed

Central Banks continue to face the challenge of bringing down inflation while avoiding a recession. They also must ensure financial stability and avoid a situation such as the failure of regional US banks in Q1 2023. The three main regional drivers of growth are the US, Europe (including UK) and China. The US reported annual real GDP growth of 4.9% in Q3 2023, well ahead of the Fed’s own estimate of long-term real GDP growth of 1.8%. Growth in China remains healthy, with the IMF forecasting China’s real GDP growth in 2024 of 4.6%. However, the picture in Euro Area and the UK is less robust, with the IMF forecasting growth of less than 1% in 2023 and an only modest recovery in 2024. These differences illustrate the importance of using an asset allocation framework that can adjust for regional settings.

Investors face three outcomes for economic growth. First, a hard landing, which is a contraction in economic activity, sharply rising unemployment, and a collapse in consumer spending. Second, a soft landing, with a gradual slowing of growth, a recession avoided and a moderate rise in unemployment. Third, no landing, with economic growth continuing at the current rate. The first outcome would imply we should reduce equities and add to longer duration bonds, given the likelihood that interest rates would then be cut significantly. If the third were to materialise, we should add to equities and reduce more defensive assets such as fixed income. Over the course of the year, the soft landing outcome has become more likely but far from certain, so we aim to maintain a balance within portfolios for investors.

Bonds: income is back

Over the course of the past two years, the rise in bond yields has meant that bonds can once again provide a counterbalance to other asset classes within portfolios. This increase in yields available from longer dated bonds gave us the opportunity to increase slightly the duration within the bond portfolios, thereby locking in higher yields. We believe it is too soon to increase duration significantly though, given the risk that inflation may persist for longer. Within corporate bonds we continue to prefer higher quality investment grade bonds over the more speculative high yield, as we believe the additional yield available does not adequately compensate us for the additional risk of the latter.

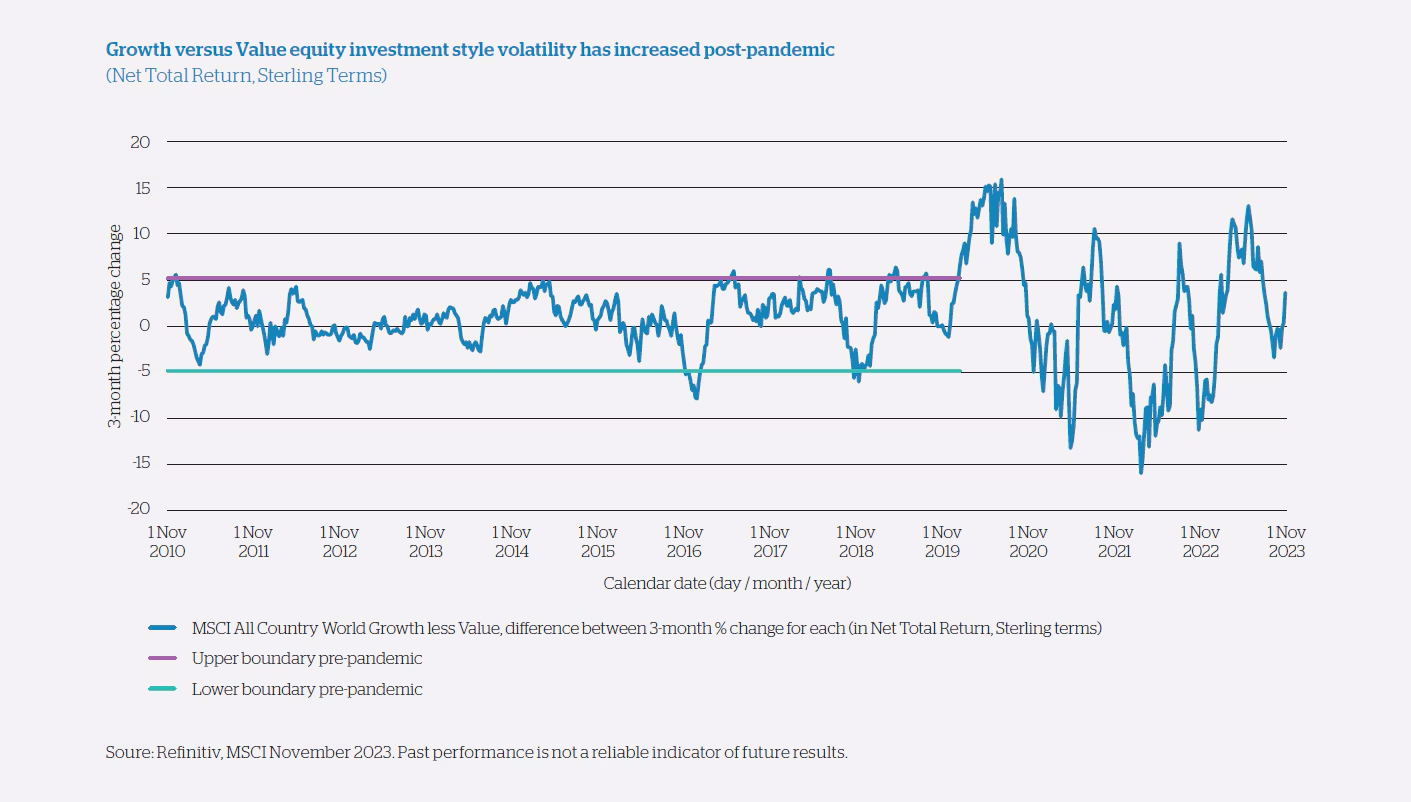

The equity barbell remains in place

The graph below shows how, since the pandemic, the style leadership of the equity market has changed more frequently and become more pronounced. For this reason, we have implemented a barbell approach in the equity portfolios, whereby we aim to achieve an equal weighting of both value and growth investment styles. Given the range of possible economic scenarios together with current heightened geo-political risks, the barbell approach remains. Despite this balance, we continue to take conviction views on a geographical basis, emphasising the different investment styles through our core equity and thematic exposures.

Conclusion

As we weigh up the investment outlook, the challenge for asset allocators is how to take a calculated position to keep exposure to more than one economic scenario materialising. There is currently insufficient visibility for us to back a single sustained outcome. Instead, staying invested but keeping balance continues to be our goal.

Related articles

Request an initial consultation

Request an initial consultation

If you have any questions or would like to get in touch, submit a call back request and our team will reach out.

Get in touch

Get in touch

or call us on: 020 7499 6424

or email us at: [email protected]